RISD MFA

Graduation 2021

Duration: 3 Years

Graduation 2021

Duration: 3 Years

3 X $70,560

Rosanne Somerson

President of RISD

Jeffrey R. Noordhoek

CEO of Nelnet

Michael S. Dunlap

Chairman of Nelnet

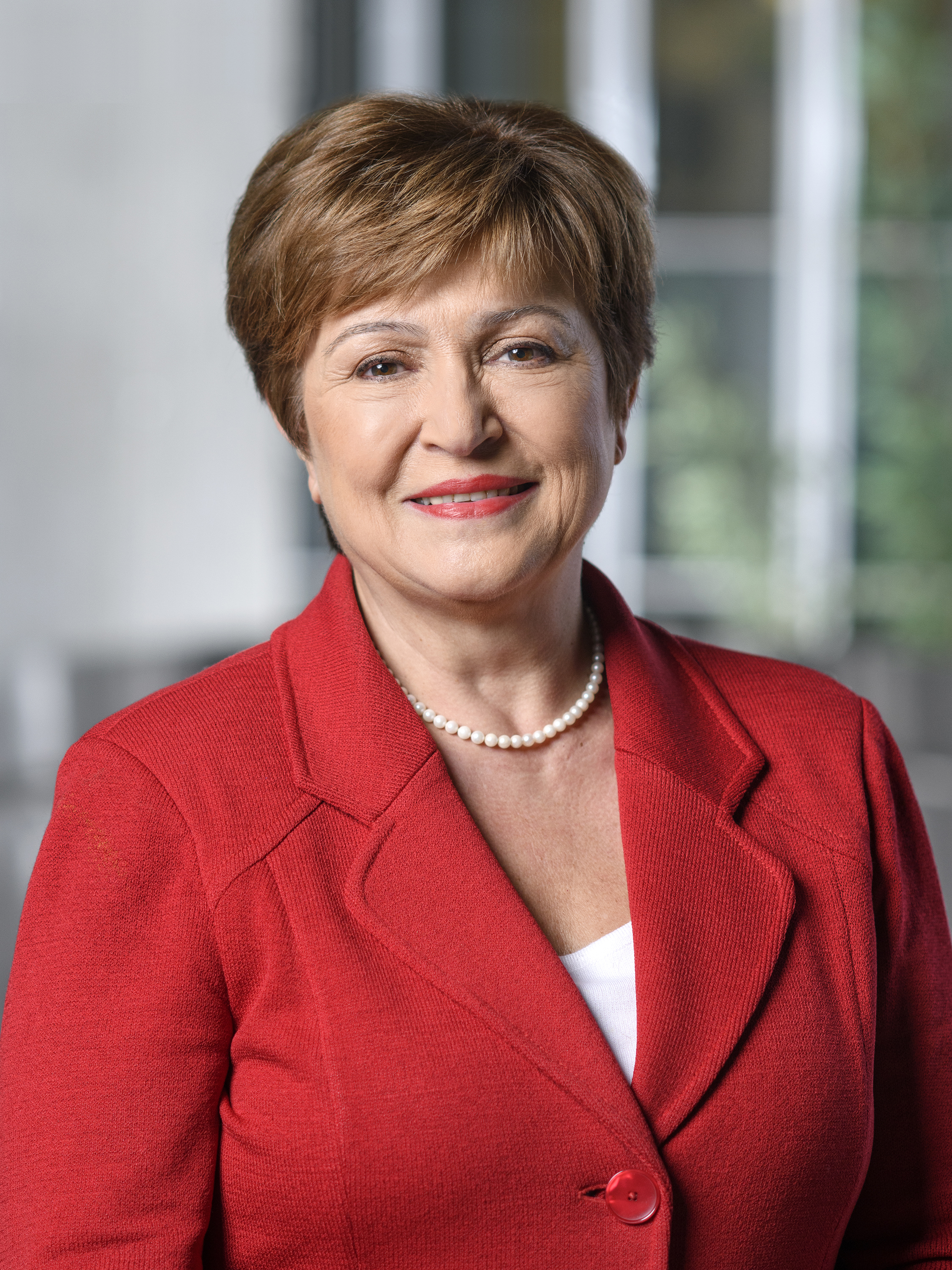

Kristalina Georgieva

Managing Director of the IMF

It's difficult to remember that the US Dollar is made of textile, not paper. That it can be stamped out in the U.S. Bureau of Engraving and Printing. That threads laden with microscopic symbols might be woven into the cotton pulp. That a glyph, the EURion, might make the forms unscannable. That the pyramid meant something to someone. That the ink might stain your fingertips. Currency is a collectively agreed-on fiction, but that seems uncomplicatedly true. What's far stranger, and perhaps more illuminating, is how little human investment we have in the craft of that fiction.

Initially, this may seem like a bold claim (especially considering the pressing character of money), but really consider a dollar bill, or an invoice, or a contract—do you really feel anything for their particular arrangements of glyphs ? Does the eye of Divine Providence mean anything to you? It means nothing to me. We're living in a post-gold standard world, one turgid with speculation and symbolism. In its financialized space, the US dollar acts as a fiat cipher, a marker of how alienated we are from the material of life.

Glyphs, here, have only residual energy; to adopt David Graeber's language, these flat, beziered arcs capture the folding of "human devotion...into numbers once again"(387). The graphic ephemera of debt in America means nothing but demands endless tribute. These loosed signifiers circulate across ATMs, computers at Great Lakes Student Loans, banks, and student financial services.

Yap Stone

ca. 500 AD

Gold stater

ca. 323/2–315 B.C.

Gold aureus of Julius Caesar

46 B.C.

Rosetta Stone

196 BC

Metalor

$6,337

Repudiation of Russian Debt

$6,337

Zheng He

1371

New York Treasury Bond

1869

Treasury Note

1985-86

The US Dollar Note

$100

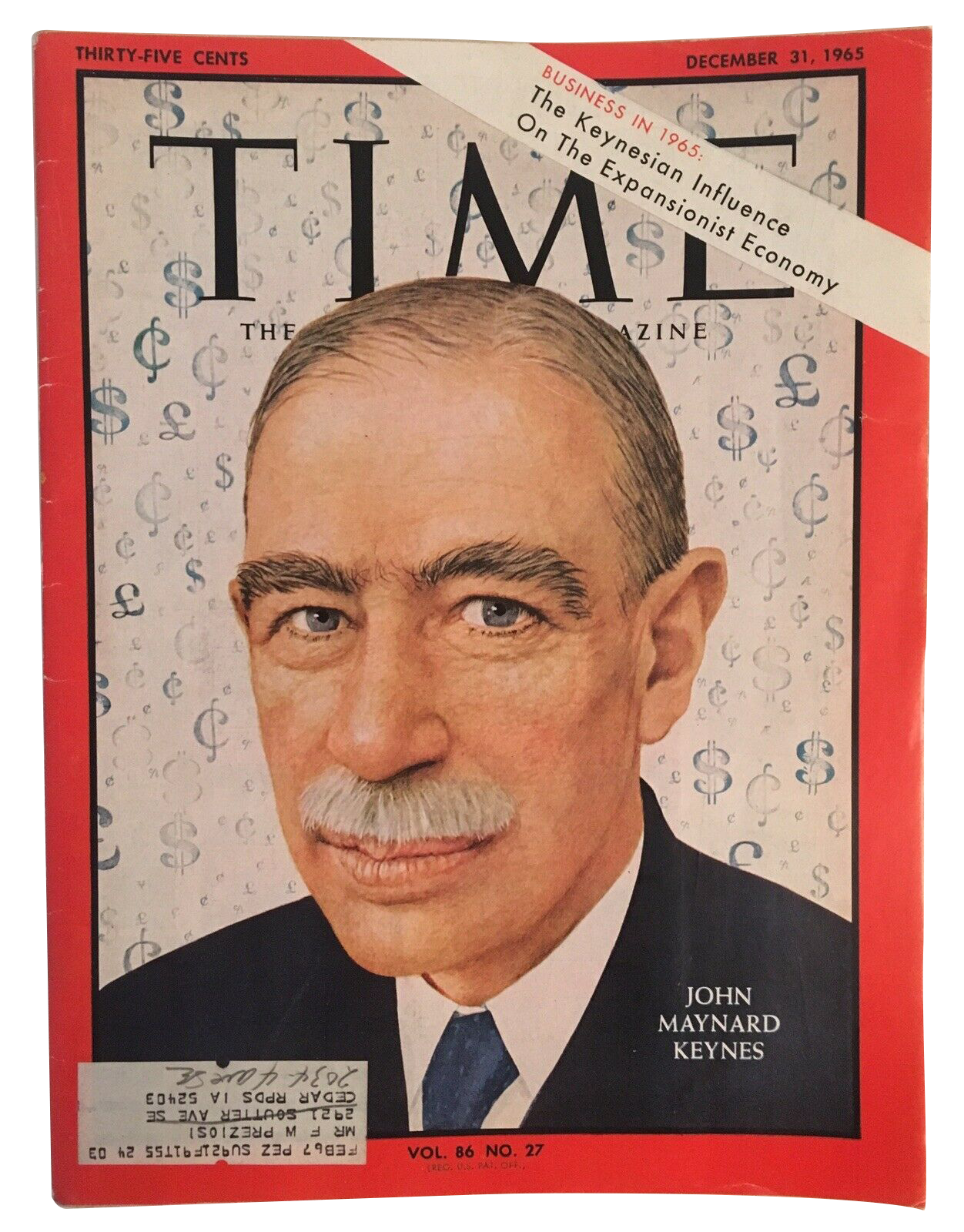

John Maynard Keyes

1985-86

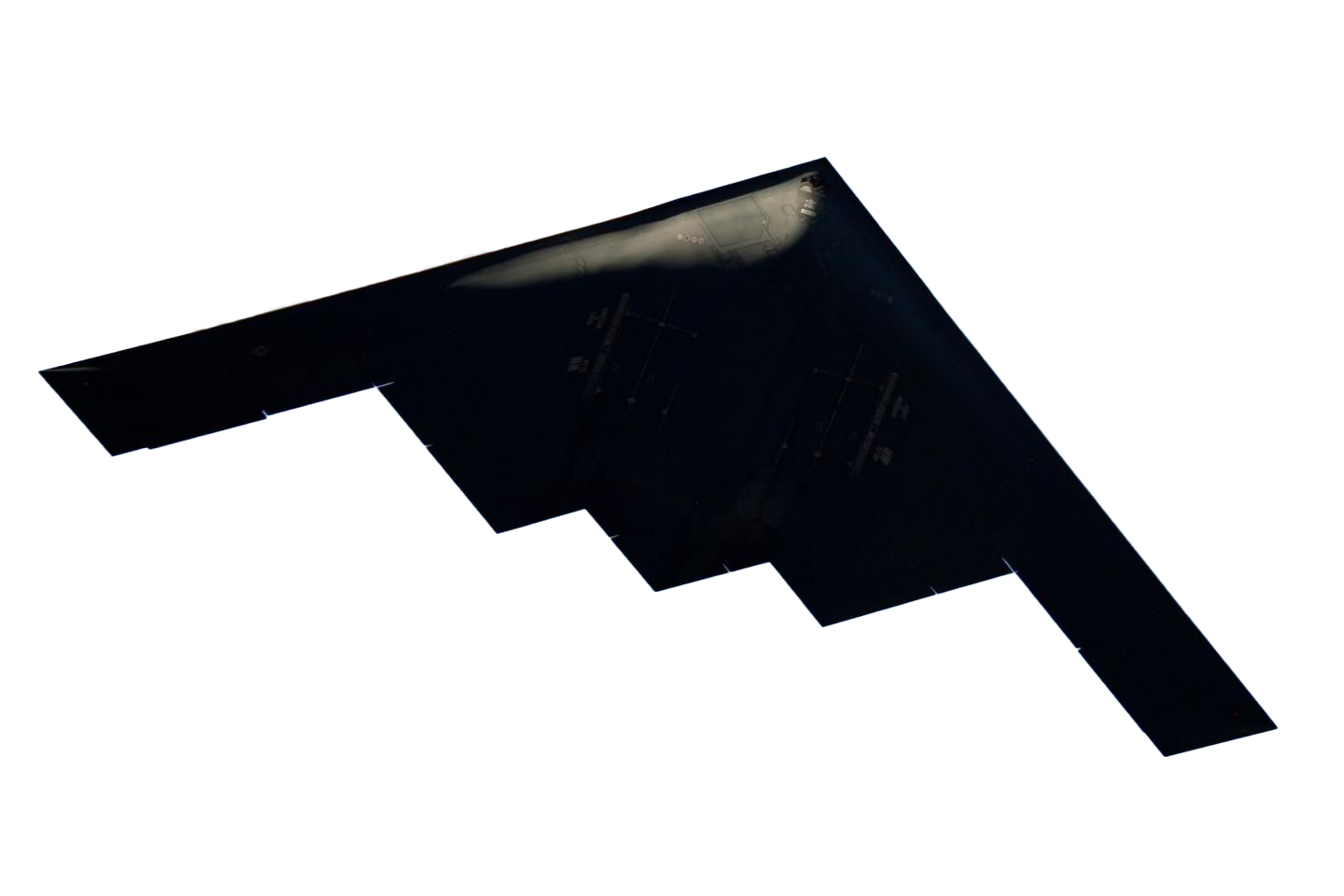

B-2 Spirit

$737 million

Kratos XQ-58 Valkyrie

$3 million per unit

.png?v=1603164543045)

“We owe David so much,” the filmmaker and debt organizer Astra Taylor told me, noting immediately how he would have disapproved of using the language of obligation to encapsulate his life’s work. Graeber had a long and distinguished career as both an activist and academic when the publication of his magnum opus, Debt: The First 5,000 Years, and his work helping organize Occupy Wall Street in 2011 made him that rare thing: a serious scholar and organizer who garnered respectful profiles in Bloomberg Businessweek and the Financial Times. He spent the last decade-plus at Goldsmiths and the London School of Economics after Yale controversially cut him off from tenure, which he suggested was due to his being “quite active in the Global Justice Movement and other anarchist-inspired projects.” “The thing to understand about David is that he really was someone who equally had a foot in social movements and intellectual scholarly production,” Taylor said. “There are people who are known as leftists through their writing and the internet and never do anything that qualifies as organizing.” One-handed shearing for more precise cuts and more precision. All with 30% less force. Don’t miss this content from our sponsor Ad by The Home Depot Graeber was a link not just between grassroots movements and the academic world, but between generations of leftist social movements. He was a veteran of the anti-globalization protests in the 1990s who helped start Occupy, one of the facilitators of a debtor movement that would influence the policy agendas of Elizabeth Warren and Bernie Sanders. He was a supporter of the United Kingdom’s anti–tuition fee protests in 2010, which would be the seed of the Momentum movement and Jeremy Corbyn’s ascendance to the leadership of the Labour Party. The question Debt sought to ask was one that seemed natural in the wake of a debt crisis that would claim millions of homes and thrust much of the industrialized world into first a sharp economic crisis, then a self-destructive series of austerity measures designed to stem the tide of sovereign debt. What was debt? What was its history, where did it come from, and how did it take such a central role in our personal and economic lives? Why was our language of obligation and morality the same as the one used to describe our credit card bills? Why does the Lord’s Prayer ask God to “forgive us our debts as we also have forgiven our debtors”? To even begin to answer this question, Graeber had to start with money and the bad history used to explain it. Generations of archaeologists, anthropologists, and historians had tried to find the origins of money (John Maynard Keynes referred to his own studies of money as his “Babylonian Madness”), but economists, especially in their textbooks, resorted to fancy. Watch this quick video for more information This advertiser wants to share this with you Ad by Sponsor See More These just-so stories about how money emerged from barter can evoke a kind of childish primitivism (“You have roosters, but you want roses,” one textbook says) or use imaginary historical examples. Even the stalwart progressive Joseph Stiglitz uses “what appears to be an imaginary New England or Midwestern town,” Graeber writes, to explain how money can replace barter, in the form of farmer Henry selling his firewood to “someone else for money” and then buying shoes from Joshua. What was debt? What was its history, where did it come from, and how did it take such a central role in our personal and economic lives? Graeber, in contrast, identifies the origin of money as “the most important story ever told” for economists, tracing it back to Adam Smith’s Wealth of Nations and even to Aristotle. This was “the great founding myth of economics,” he writes, that money was not in fact the creation of governments. It followed that economics was its own form of inquiry, separate from other ways of thinking about social life. Graeber points out this account “has little to do with anything we observe when we examine how economic life is actually conducted, in real communities and marketplaces, almost anywhere—where one is much more likely to discover everyone in debt to everyone else in a dozen different ways, and that most transactions take place without the use of currency.” Whereas the traditional account puts barter before money and money before debt, Graeber reverses this, noting that barter tends to only emerge in pre-industrialized societies when exchange happens outside of a familiar cultural context.

NUMBER OF VOTES: 831,407

NUMBER OF VOTES: 309,670

NUMBER OF VOTES: 306,294

NUMBER OF VOTES: 267,809

NUMBER OF VOTES: 203,016

NUMBER OF VOTES: 203,016

NUMBER OF VOTES: 152,165

Rebecca Solnit: So lovely to see you all here. And totally thrilling to see my favorite political thinker and political inspiration, David Graeber—someone I just find extraordinarily original and refreshing and really brilliant, partly because he’s articulating from an anarchist point of view things that don’t get discussed a lot. And maybe from an anthropological point of view—there’s a wonderful sense, I think, of “Let’s look at your curious customs,” which we used to do to the other, and now anthropologists can do to ourselves as well. And it’s very much what happens in Debt: he looks at medieval Chinese Buddhist monk debt, the origins of money in Mesopotamia, and everything from Ernest Thompson Seton’s bad childhood. It ends up giving us incredibly powerful tools to think about who we are and what we’re doing now in our global, national, and personal relations.

One of the funny things about the Occupy movement is that people really want individuals and leaders, and David got saddled with the task of being one. Even so, it’s been very exciting—one of the things that Occupy has done, “End Debt,” has made David very visible. He was not so visible before. Fragments of an Anarchist Anthropology was the first book of his that I came across. If you’re like me and you feel like you should never not have a book with you, and you’re not always ready to carry Debt, make sure you have Fragments with you, which is as fresh and original and as exciting and eye-opening in its analysis. So David, are you so mortified that I should just keep talking, or is there anything you want to refute yet?

David Graeber: Not so far—you’re OK.

Rebecca Solnit: Clearly Debt was brewing for a long time. Was there something in particular that got you focused on the subject?

David Graeber: A bunch of things. More than anything else, it was really the realization of the tremendous moral power of the idea of debt.

I was at Westminster Abbey—for this strange reason I was actually living in Westminster Abbey for a month and a half. I was at a garden party and the priest—who was a nice person, but slightly annoying—had this habit of introducing me to everybody by saying, “Hello, this is David Graeber. He’s an anarchist.” Really limited my possibilities for these conversations. To this one person, he said, “This person is an activist like you; you’ll have a lot in common.” It turned out it was this lawyer who’s an activist involved in various community campaigns. Nice person. I was telling a story about the “Drop the Debt” campaign and about the global justice movements I was doing, and I don’t know if she was just playing naive or if she actually didn’t know, but she asked, “What’s that about?”

I told her the story about Madagascar and how, with the IMF structural adjustment policies, they had to do these budget cuts, and one thing they had to cut was the malaria eradication campaign—they couldn’t afford to keep it up. Malaria returned to the highlands where it had been eradicated for fifty years. They thought they had immunity, and at least ten thousand people died. Five thousand of them were children. I was telling her this and she asked what we could do about it and I said, well, we could just drop the debt. Suddenly she said, “Well, they borrowed the money, I mean surely they should have to pay their debts.” And it struck me: in what other circumstance would a nice person just spontaneously defend the death of five thousand babies? What is it about the moral power of debt that makes people willing to accept things that they would probably not accept under any other circumstance? And I started thinking about it and realized that nobody’s ever written a book about the history of debt.

Rebecca Solnit: The research was kind of amazing. But it wasn’t really until the website, “We Are the 99 Percent,” where people started telling their stories of indebtedness that I realized just how extraordinarily brutal debt has become as a force in society today, whether it’s healthcare debt, mortgages—particularly on houses that have gone underwater—or college debt. All these different forms of indebtedness have essentially created a new form of debt peonage, and I think they’re talking about bringing back debtor’s prison.

David Graeber: In several states, they are locking people up for failure to pay. Usually, if it’s court mandated, they can get into court for not paying. Well, the “We Are the 99 Percent” website, I was actually looking at that the other day because in theory I’m supposed to write a book on Occupy Wall Street. It’s fascinating, that page. The interesting thing for me was that this book came out in July and I was in New York. I had a year off and I had two projects. One of them was working with the Occupy Wall Street stuff, which was in formation at the time in August, and I was writing the book. I tried not to put them together so I didn’t talk about the Occupy stuff at the book events and I didn’t talk about the book at the Occupy events. But it was hard not to because every time I did any kind of event about the debt book and there were people under the age of twenty-five in the audience, two or three would come up afterwards and start saying, “Is there any way that we can start some sort of campaign about student loan debt?” And I’d start hearing these stories that were completely horrific. So I realized that there was something out there.

And the “99 percent” thing fascinated me, too. It actually helped me a little bit because one of the things I was trying to figure out was the changing class lines that Occupy represents. The fact that the working poor are the people suffering out subprime mortgages and fatal loans and more and more of our money—you know, capitalism is operated by extracting money, not so much directly being paid. When I was in college, that’s what they called it. The difference between capitalism and feudalism is that under capitalism, they make money directly through wages, manufacturing, and commerce and under feudalism, it’s directly through juro-political means. Seems to me that, what, 16 percent of profits to emerge from corporations are not from any kind of premium? And that’s to overstate it, because even car manufacturers aren’t getting all the profits from their financial transactions.

Rebecca Solnit: So, you’re saying we’re heading towards feudalism economically?

David Graeber: Something like that. You know, there was this big discussion on the internet that included me quoting Sir Moses Finley saying that in the ancient world, there is basically one revolutionary program: cancel the debts and redistribute the land. And they’re saying that basically we’re back to that.

Rebecca Solnit: In a piece from one of my disaster magazines, an anthropologist went to Kenya and an affluent herdsman offered to kill a goat and roast it for a feast in his honor. The anthropologist said, “Oh, that’s great, thank you so much. What a great compliment.” And then the herdsman borrowed the goat from a really poor guy and the anthropologist asked, “What are you doing?” It took him another year of being in the community to realize that the herdsman was creating a web of mutual—I’m trying to avoid using the horrible financial language that is so reductive—but essentially, that the rich man now owed the poor man something that the poor man could collect when times got tough and it pulled him into the community, it connected him. In fact, by taking something material away from the poor man, the herdsman was giving him something immaterial that was worth more; he wouldn’t lose materially in the long run and he would gain immaterially.

But what’s also interesting about these narratives is something that they both clarified for me: that part of the function of money is to seal off. You want my house, you give me money, I go away, and all of our relations are severed forever. I wondered if you would talk about how money changing hands becomes a way to sever a relationship, the certain mutual times in which money didn’t sever, the ways in which we don’t have to think of it as debt because it doesn’t have to be closed, sealed, and finished, and that maybe it’s not even a bad thing to be in somebody’s debt (which is now wholly a bad thing).

David Graeber: An anthropologist who studied people in central Nigeria showed us how we were completely clueless. She doesn’t really speak the language and she gets a house, and immediately women start showing up from the neighborhood and dropping off little baskets of stuff: somebody bringing some okra, somebody bringing some fish. And she doesn’t know what to do so she takes out her little notebook and eventually somebody takes pity on her and starts explaining how things work. The person says, “Well, you know, you give something back to these people. But the key is you have to figure out exactly what it’s worth, and then give them either something slightly more valuable, or slightly less valuable. So if it’s worth twelve shillings, you give them something worth eleven or thirteen, never give twelve. Because if you give twelve, that’s like saying, ‘go to hell, I don’t ever have to see you again.’” So everyone has to be a little bit beholden.

This is a society where there are all these kinds of transactions, but they’re consciously trying to resist the idea of closure that money makes easy to introduce. Similarly, one of the fairly interesting things about money is that it makes certain things possible that wouldn’t be possible otherwise—it doesn’t make them inevitable. Hence the strange blindness of economists to what would actually happen when one does exchange things if there isn’t money in such contexts. The fascinating thing about standard economic stories is exactly that: they assume that everybody wants that kind of closure. That all human relations are forms of exchange, because if everything is an exchange then it’s true that we’re both equals. We walk up, I give you something, you give me something, and we walk away. Or I give you something, you don’t give me something right now, and you owe me. So if we have any ongoing relationships at all, it’s because somebody is in debt.

However, the problem with that is that debt—like sin—implies that one party in the transaction didn’t live up to expectations, at least in the moment, and has done something wrong. In a lot of moral and religious versions of this, probably both parties did. And the implication—if you assume that human relations are all manners of exchange, which throughout the history of commercial society people have wanted to think—is that you end up thinking that there is something wrong with social relations. People don’t have an ongoing relation unless it’s a form of debt because everything is an exchange, so ongoing relationships are incomplete exchanges, and therefore one party is probably to blame—more likely than not, both are. Sociality itself seems to become like a matter of sin, and inherently wrong.

Rebecca Solnit: Wait, how does sociality become a sin?

David Graeber: Because if you imagine that everything is an exchange, then we’re supposed to just transact and walk away. If we haven’t walked away and we still have a relationship, it’s because there’s a debt.

Rebecca Solnit: One of the things that has come up for me is how we talk as though we live in a capitalist society. I often think that the reason capitalism hasn’t completely destroyed everything is that a huge amount of anti-capitalist endeavor goes on, from labors of love, nurture, friendship, and barter to gift economies and different kinds of exchanges, not just one alternate model but a whole host of other ways in which we engage with each other and with the world that aren’t financial and debt-based. For example, the oil corporations spend a lot of money to get, say, the tar sands pipeline through, but nobody’s—you know, there are definitely environmentalists being paid—but a lot of people are acting for something other than financial compensation. So if the tar sands pipeline doesn’t get made, it’s because a huge amount of people are doing something that doesn’t involve remuneration, money, etc., because we’re not actually the self-interested financial instruments that economists like to imagine we are.

David Graeber: David Harvie, not the British, Marxist, geographer-type guy, but David Harvie, the British Marxist economist, actually calculated how much time people in the U.K. spend on labor to get money, versus labor on something not oriented towards money and it comes out at about fifty-fifty. So even in the most market-obsessed society, we’re still spending half of our time on something other than just getting cash. It is really important to emphasize that, because we have a tendency to take this totalizing view that by capitalism, anything that serves to reproduce capitalism is capitalism, and that’s all that’s important about it. And if you do that, how can you possibly imagine capitalism ever not absorbing everything. There’s also this notion that capitalism is like this fractal thing where anything that contains an element of capitalism anywhere inside it is just something that turns into capitalism. It is an incredibly defeatist attitude. One of the things I was trying to show in the book is that if you choose to look at reality that way, I suppose you can, but you have to do enormous violence to reality to do so consistently.

For example, the notion that anything that money touches, or that commerce touches, or that exchanges trade, is capitalism, and if you introduce any element of that into what might seem to be a non-capitalist situation, then suddenly that is part of capitalism. One of the things I discovered while writing this is that, to the contrary, markets and state power have always been deeply intertwined. And one of the facts that I discovered while researching, which I didn’t know at all before I started writing, is that free market ideology—does anyone know where it first comes from? It comes from medieval Islam, and specifically, Shari’a. Because Shari’a provided this commercial law that is independent from the state.

It made it possible. There are markets extending from Mali, Indonesia, way outside the purview of any one government which operated under civil laws, so contracts weren’t, except on trust. So they have this free market ideology the moment they have markets operating outside the purview of the states, as prior to that markets had really mainly existed as a side effect of military operations. Coinage systems were created to pay soldiers. So this market system outside of the state immediately starts transforming entirely—Adam Smith actually took all his best ideas and lines from sources from medieval Persia. But one thing he doesn’t take is the underlying assumption they have that the basis of a market is mutual aid.

You know, competition has a role, they don’t deny that. But that’s not what it is all about. It makes sense, because you can’t have cutthroat competition when there’s no one stopping you from actually cutting each other’s throats. In order to build up trust we also have to think about each other’s needs and it creates an entirely different dynamic. So in a weird way, they see the market as an extension of communism. In a way like mutual aid: we need each other to do things that we can’t do for ourselves. If we are intimately connected with each other, we just give things to each other; if we don’t know each other we find another way to handle it. If you think about it, each according to his or her abilities and each according to his or her needs is sort of the same thing as supply and demand.

When you take away the violence from the market, even it starts shifting into something else—not exactly paradise, but it doesn’t become the market in the way we see it now. The conclusion that I ultimately came to is that certain types of communism—I think we should just change our use of the term. Now, we’re used to thinking of communism as being once-upon-a-time-all-things-were-owned-in-common, maybe-someday-this-will-come-again. And people agree that there is a sort of epic narrative going on here. I think we should just throw this narrative out, it’s irrelevant anyway, and who cares who owns things? I don’t. You know, we all own the White House. So what? I still can’t go in, right?

The question is: who has access to it under what circumstances? And if you look at it that way, where the idea of each according to his or her abilities and each according to his or her needs applies, all societies are based on a sort of minimum level of communism. Otherwise, you couldn’t have any social relations at all.

Communism is the basis of all sociality and it’s the basis of cooperation. Within a capitalist corporation, someone says, “Lend me a wrench,” and someone asks, “Yeah, what do I get?” You assume that the idea of each according to his or her abilities, each according to his or her needs—in solving a problem—is actually the only thing that works. And in situations of disaster, there are often communistic notions of improvisation, where you basically exchange hierarchies and all of a sudden all those things that are luxuries that you can’t afford, you have them in an emergency. So I think we need to think of capitalism as a very bad way of organizing communism. Much of what we do is already communism, so just expand it.

Rebecca Solnit: One of the things that’s really present in your work is that life after the binaries, whether state socialism or free market capitalism. I wonder if you want to talk about some of the ways that anarchist ideas and anarchist values have become more and more the norm and the status quo without being acknowledged, and where you see that going?

David Graeber: Status quo in what circles?

Rebecca Solnit: Ours. And if you want to expand them, all of the insurrectionary activity of the last twenty or thirty years. But just when you look at the decentralized, non-hierarchical organization of the Egyptian uprising, of the Occupy movement, of the anti-globalization movement and the shutdown in Seattle, and a lot of stuff where people almost take it as a matter of course that we’re not going to have hierarchy and we’re not going to obey leaders and that our vision of a better world does not include some kind of total control of resources by corporations. We’re against them being controlled by corporations, but that doesn’t mean we want them controlled by the state. Just for starters.

David Graeber: You just said it better than I could have. Anarchism is surprisingly effective in solving actual problems largely because anarchists have thought a lot about solving actual problems on a micro level in ways that other political ideologies don’t really feel they have to until after they seize state power.

Rebecca Solnit: Have they thought about it, or have they just described the way that things actually work well in the kinds of societies that people like?

David Graeber: So in a way it’s saying that people—actually anarchist center groups and a lot of people who call themselves anarchists who are working on principles that I would identify as anarchist—but then again I’m not going to call them that… For me, it does seem intellectually honest.

Maybe it’s because I do come from an academic milieu where you quote your sources, but just to deny where you’re getting these ideas from seems like you’re trying to pull something over on people. Other people whose job is, say, community organizing, may not want to bring it up either, and I respect that.

Rebecca Solnit: But don’t you yourself say that a lot of what could be identified as—if you look at a lot of traditional societies, they’re all organized along what we might call anarchist guidelines, but it’s not like the Zapatistas were reading European social theory.

David Graeber: Well, some of them were.

Rebecca Solnit: Well, OK, some of them were, the tall, green-eyed one. But that’s what I’m trying to get over: the idea that anarchism offers a description of equitable relations that go way back rather than a hypothesis of what the future should look like.

David Graeber: Right, and it seems silly to say that there were Marxists in Han, China. But there were definitely anarchists in Han, China. In fact, you could even make an argument that the school of the Tillers was actually trying to create utopian communities in these sort of free spaces between various little wards or principalities. They had this idea that the only leadership was by example, and they sought to draw people from surrounding kingdoms and gradually create an egalitarian society.

It’s actually quite fascinating because they were a major social movement of that period; there were all sorts of curious social movements going on. Eventually, people started taking up similar ideas in court and that’s how you got stuff like, say, this weird anarchistic advice to princes. But when it hits the cities and the intellectuals, suddenly we have all these individualists and primitivists strings. And you know, this is 300 BC, exactly the same pattern you see elsewhere. So there is something really fundamental that seems to crop up at the same time in different places.

I once put out the idea that the best way to think about anarchism is as a combination of three levels. On the one hand, the sort of instinctual revulsion against forms of inequality in power; on the other hand, a reappraisal of what one is already doing in egalitarian relations; and then the projection of these principles on all sorts of relations. So those three moves making what you’re already doing self-conscious and trying to take those principles and project them to all sorts of relations… But that’s what I’m trying to do in the book and I hadn’t really thought of it until I just said that—when I say that what we’re already doing is communism. The first step we have to make is to realize that we’re already closer to it than we think. We don’t live in a capitalist totality. Capitalism couldn’t survive as a totality anyway. We live in this complex system and we already live communism and anarchism in a million forms everyday.

Rebecca Solnit: Flipping through Fragments of an Anarchist Anthropology as I inadequately prepared myself for this event, I noticed that a decade ago it seemed like you had to be kind of defensive against the anti-utopian strain that was so strong then. Do you think that we’ve reclaimed utopia through Occupy and some of the other movements?

David Graeber: I think it’s starting to happen. I think there has been a war of the imagination over the last several years. I was thinking a lot about what there might be to be optimistic about. And I came to the conclusion that this feeling of hopelessness that everybody had was a manufactured product, and that’s what neoliberalism is really about. Neoliberalism isn’t an economic program—it’s a political program designed to produce hopelessness and kill any future alternatives.

I first started picking up on it when I thought about tactics of direct action. What is this incredibly bizarre, preemptive attitude that the people in power have? Why do they take us more seriously than we take ourselves—basically, the entire Iraq War was designed around heading off an effective antiwar movement. It seemed much more important to head off an effective antiwar movement to get over the Vietnam war syndrome than it was to win the war. They had these rules of engagement, they had all these formulas: how many dead bodies, how many protestors? They came up with these rules of engagement which guaranteed that lots and lots of Iraqi and Afghan civilians would get killed, but very few of our soldiers. This ensured that they couldn’t possibly link… But they didn’t care, because it was more important to be allowed to have a war successfully than to win the war. The key thing is to preempt the resistance at home.

If you look at a lot of the things they do, it suddenly started to make sense. Why is it that they’re willing to shut down the IMF meetings so we can’t? It’s the same thing—because they found out about it. They meet people who are going to meetings, and we’re all frustrated and totally overwhelmed by a massive police presence. After the first one on May 16th, I had friends who had friends who were actually at the meetings and they were saying that everyone’s complaining: “This totally sucks,” “They shut down half the meetings,” “All the parties are shut down everywhere,” “We can’t get around,” “We can’t actually meet at all.” We basically canceled the thing. But the point is, we weren’t supposed to know that. We were supposed to think it was ineffective. So they don’t care if the IMF meets, they care that we don’t shut it down.

So what is this obsession they have with us never feeling we’ve actually accomplished something? And I thought: everything in neoliberalism can be thought of in that sense. Look at labor policy. What’s the point of making everybody work too much? It’s not very useful. It is destroying the planet, actually. But it’s great at keeping people off the streets. What about precarious labor? It’s actually not the most efficient form of labor at all. They were much more efficient when they had loyalty to their workers and people were allowed to be creative and contribute—you know that what precarious labor does is that it’s the best weapon ever made to depoliticize labor. They’re always putting the political in front of the economic.

Another example that struck me was the example of the Soviet Union. You would think that if neoliberals were in any way honest, after the collapse of the Soviet Union the first thing to do is get rid of the Red Army and the KGB, and build up the economy. Instead, they just get rid of the economy and keep the military and the KGB. Ideological conformity, this sort of guard labor to keep control, is what it’s all about. It’s not about economic policy at all. The example of Russia reminds us that keeping up that enormous dead weight of the security apparatus required to enforce the ideological conformity to preempt anything that looks like an alternative or a social movement is destroying capitalism.

They can’t afford it. That’s why they have these economic crises and speculative bubbles and collapses. You can connect the dots in various ways. The thing is sinking under the dead weight of the apparatus they’ve created to make it seem inevitable. So we’re in this weird situation where the only really effective thing done in the last thirty years on a global level has been to convince us that no other economic system could ever be possible. Now suddenly the one we’ve got is completely falling apart and everybody is like “Oh no, what are we going to do now? Nothing else is possible, what are we going to do?” And so this is the quandary of our time. For a while, the utopian thing was out but it seems like we need to get back to it because the hopelessness can’t hold out forever when right before our eyes it’s falling apart.

Rebecca Solnit: I feel like it’s back in a lot of different ways. When I started working on disasters, one of the things that I ran into immediately was the assumption that the real disaster is the absence of the authoritarianism of the state. The assumption that in the absence of the system that has collapsed in Katrina or 9/11 or the bombing of Britain or what have you, we’ll fall apart somehow. We’ll fall apart morally, we’ll become rabid wolves, ripping each other up and raping and pillaging or, in the favorite word for Katrina, “looting.” Or we’ll fall apart in another way if we’re not wolves—we’re sheep, we’re going to stampede and panic and fall apart.

There was an assumption that aerial bombing of civilians in World War II would cause fragile, working-class people to basically have nervous breakdowns and it would paralyze the state. That was the logic of aerial bombing. In fact, it doesn’t happen at all, but the logic behind aerial bombing has never stopped, even though it never demoralizes, terrorizes, or paralyzes a population. But the assumption in disaster is essentially the rationale of an authoritarian state about why we need an authoritarian state—because we’re basically savage, competitive, hostile, chaotic creatures. And why we are and they aren’t and that they should run everything is an assumption I don’t quite understand.

But at the same time, it was always really interesting looking at disasters. In fact, the opposite is true: everyday life is a disaster, and disaster can liberate us. In response to what you were saying about the greater concern with controlling us than Iraq during the Iraq War, I felt like in a way all the post-9/11 stuff the Bush administration did was about shutting down that incredible moment when right next to Wall Street… One of the amazing things about Occupy when I finally went there is that everyone talked about Wall Street—it’s closer to Ground Zero than it is to Wall Street. And it felt like it was ten years and six days after the event, it picked up where we had left off. Because when then Twin Towers collapsed, nobody trampled each other, nobody panicked, all that savage social Darwinism you were promised didn’t happen. People aided each other in kind of extraordinary ways: a quadriplegic accountant was carried down sixty-nine stories by his coworkers who didn’t do any accounting for what he owed them on the way.

And then you have these amazing things: people established this kind of free circulation of goods, the commissaries that were supplying Ground Zero, and the displaced people, and things like that. You suddenly had this—you know, we had the Oakland Commune last year, we had the Paris Commune… it was like the New York Commune, there was this moment in which relations were completely different, both at a practical level but also at an emotional level. Everybody says everybody made eye contact, they cared about how you were, boundaries came down. And that was terrifying to the Bush administration and to Wall Street, which was essentially Al Qaeda’s target. And they had to get us back to business—remember that campaign, America Open For Business and all that other stuff? This is a long way around saying that what actually happens in disasters is that they demonstrate that people are actually very good at being communists in the sense that they instantly abandon capitalism, that they love these relationships of mutual aid, because the astonishing thing about disasters is that people are often weirdly joyous in them, because they’ve recovered a sense of agency, a sense of power, etc.

So I did that work, David was doing his work, and what I’ve become really interested in is mapping the bigger picture. If you look at these fields that are emerging—altruism studies and empathy studies and stuff, even in the last decade in the utopian era where everything from Buddhism to sociology to neurology to radical economics and social theory is really trying to redefine human nature and human desire in ways that I think are incredibly utopian. It turns out that we’re actually capable of something other than neoliberalism and actually we’re really capable of enjoying ourselves more than we do under neoliberalism. It feels that if neoliberalism was first about privatizing desire and imagination before the economy, then we’re in this process of publicizing it again, except we don’t have an equivalent. What’s the opposite of privatize? “Publify”? Collectivize, or something? Bringing people back into the open: both literally, with living in the streets, which is happening suddenly across the country with the revolutions in Occupy last year, but also imaginatively, with the sense of connectedness, etc.

I feel like we’re in a truly revolutionary period, not just in terms of practical activities to overthrow regimes in the Middle East or Occupy but also in terms of radical redefinitions. I feel like workers are a big part of it, but there’s so much more going on. The Bay Area has this Center for the Study of the Greater Good at Berkeley, which is a kind of altruism studies institute. And I forget, isn’t there another one at Stanford that the Dalai Lama funds? The Center for Studying Altruism and Compassion, I think? But it’s this kind of radical reconfiguring of what it means to be human, in who we are, what we want, and what we think we’re capable of. I wonder how you see your work fitting in, but also how you see Occupy fitting in?

David Graeber: Oh, I do. It’s interesting when you were talking about 9/11. What I remember so clearly because I lived in New York at the time were the parks, you know, Union Square and other parks like that. Suddenly, everybody sort of converged—much like they did during the blackout—on these public spaces and made these shrines of people who were missing. They would put flowers and candles. But every park that I was in—it was Union Square, because that was the nearest one to me—was immediately covered in peace symbols. And there were drums, basically everybody turned into a hippie. [Laughs] There were drum circles and poetry readings.

Rebecca Solnit: Why are there always drum circles?

David Graeber: Yeah, but utopianism—one comment I’d make is that when it comes to altruism, when it comes to utopianism, I think the Left is just catching up now. Because I think in a weird, perverse way, the Right figured this out before we did.

Rebecca Solnit: How so?

David Graeber: How so? Why is it that when the Right says, “We need austerity and shared sacrifice,” and then people vote for them, Democrats ask, “Well, why aren’t people voting for their own economic interests?” It’s because, in a way, Democrats are saying, “Look for us because we’ll throw you some scraps and it’s better than those other guys who will fuck you entirely.” But the other guys are saying, “We think you’re good people for the good of the country” and they’re saying, “You know, you think I’m basically rotten, and you’re even more rotten, we’re not gonna get into this.” At least those guys are saying, “I’m a good person.” And I actually had this realization about this—I wrote a piece for Harper’s—but I was trying to figure out this weird combination of right-wing populism and communism: we hate the cultural elite and support the troops. What do these things have to do with each other? Apparently, nothing. But they seem to be linked in people’s minds.

I came to the conclusion that most people in America would really like to be able to get a job where they think they’re doing something noble and nice and good and it isn’t just for the money. But the reason they hate what they call the cultural elite is that they see it as a class that’s grabbed all the jobs where you can get paid to do something that isn’t just for the money—if it’s art, if it’s charity, if it’s intellectual, if it’s political, whatever it might be. Because those are all the things where, if you want to get a job in that area, they won’t pay you for the first year or two, because there are all those unpaid internships. They see these people who grab all the jobs where you get to be good and noble. And we don’t get to do that. If your father is an air-conditioner repairman from Nebraska, its conceivable that you might become a CEO, but you can’t imagine being the drama critic for the New York Times. So if you come from a background like that and you want to actually have a career which involves doing something noble in the world, what can you do? You can join the army. That’s about it. Or you can work for the church. That explains a lot of the focus of right-wing populism. The right wing figured that out, that people want enough to survive and to do good.

Rebecca Solnit: So how do you feel about where Occupy is right now?

David Graeber: I think there was a real crisis period after the eviction. There was a lot of disruption; the larger meeting became incredibly dysfunctional for about a month. It’s really gotten better, and people are starting to refocus. And I think people are getting really excited about things that are going to be happening.

When the Venetian merchant Marco Polo got to China, in the latter part of the thirteenth century, he saw many wonders—gunpowder and coal and eyeglasses and porcelain. One of the things that astonished him most, however, was a new invention, implemented by Kublai Khan, a grandson of the great conqueror Genghis. It was paper money, introduced by Kublai in 1260. Polo could hardly believe his eyes when he saw what the Khan was doing:

He makes his money after this fashion. He makes them take of the bark of a certain tree, in fact of the mulberry tree, the leaves of which are the food of the silkworms, these trees being so numerous that whole districts are full of them. What they take is a certain fine white bast or skin which lies between the wood of the tree and the thick outer bark, and this they make into something resembling sheets of paper, but black. When these sheets have been prepared they are cut up into pieces of different sizes. All these pieces of paper are issued with as much solemnity and authority as if they were of pure gold or silver; and on every piece a variety of officials, whose duty it is, have to write their names, and to put their seals. And when all is prepared duly, the chief officer deputed by the Khan smears the seal entrusted to him with vermilion, and impresses it on the paper, so that the form of the seal remains imprinted upon it in red; the money is then authentic. Anyone forging it would be punished with death.

That last point was deeply relevant. The problem with many new forms of money is that people are reluctant to adopt them. Genghis Khan’s grandson didn’t have that difficulty. He took measures to insure the authenticity of his currency, and if you didn’t use it—if you wouldn’t accept it in payment, or preferred to use gold or silver or copper or iron bars or pearls or salt or coins or any of the older forms of payment prevalent in China—he would have you killed. This solved the question of uptake.

Marco Polo was right to be amazed. The instruments of trade and finance are inventions, in the same way that creations of art and discoveries of science are inventions—products of the human imagination. Paper money, backed by the authority of the state, was an astonishing innovation, one that reshaped the world. That’s hard to remember: we grow used to the ways we pay our bills and are paid for our work, to the dance of numbers in our bank balances and credit-card statements. It’s only at moments when the system buckles that we start to wonder why these things are worth what they seem to be worth. The credit crunch in 2008 triggered a panic when people throughout the financial system wondered whether the numbers on balance sheets meant what they were supposed to mean. As a direct response to the crisis, in October, 2008, Satoshi Nakamoto, whoever he or she or they might be, published the white paper that outlined the idea of Bitcoin, a new form of money based on nothing but the power of cryptography.

The quest for new forms of money hasn’t gone away. In June of this year, Facebook unveiled Libra, global currency that draws on the architecture of Bitcoin. The idea is that the value of the new money is derived not from the imprimatur of any state but from a combination of mathematics, global connectedness, and the trust that resides in the world’s biggest social network. That’s the plan, anyway. How safe is it? How do we know what libras or bitcoins are worth, or whether they’re worth anything? Satoshi Nakamoto’s acolytes would immediately turn those questions around and ask, How do you know what the cash in your pocket is worth?

The present moment in financial invention therefore has some similarities with the period when money in the form we currently understand it—a paper currency backed by state guarantees—was first created. The hero of that origin story is the nation-state. In all good stories, the hero wants something but faces an obstacle. In the case of the nation-state, what it wants to do is wage war, and the obstacle it faces is how to pay for it.

The modern system for dealing with this problem arose in England during the reign of King William, the Protestant Dutch royal who had been imported to the throne of England in 1689, to replace the unacceptably Catholic King James II. William was a competent ruler, but he had serious baggage—a long-running dispute with King Louis XIV of France. Before long, England and France were involved in a new phase of this dispute, which now seems part of a centuries-long conflict between the two countries, but at the time was variously called the Nine-Years’ War or King William’s War. This war presented the usual problem: how could the nations afford it?

King William’s administration came up with a novel answer: borrow a huge sum of money, and use taxes to pay back the interest over time. In 1694, the English government borrowed 1.2 million pounds at a rate of eight per cent, paid for by taxes on ships’ cargoes, beer, and spirits. In return, the lenders were allowed to incorporate themselves as a new company, the Bank of England. The bank had the right to take in deposits of gold from the public and—a second big innovation—to print “Bank notes” as receipts for the deposits. These new deposits were then lent to the King. The banknotes, being guaranteed by the deposits, were as good as gold money, and rapidly became a generally accepted new currency.

This system is still with us, and not just in England. The more general adoption of the scheme, however, was not a story of uninterrupted success. Some of the difficulties are recounted in James Buchan’s fascinating “John Law: A Scottish Adventurer of the Eighteenth Century.” Law was the Edinburgh-born son of a goldsmith turned banker. He moved to London in 1692, where he observed the wondrous new scheme of government paid for by long-term debt and paper money. One of the most significant effects of the paper money was the way it stimulated borrowing and lending—and trading. Law had an instinctive understanding of finance and a love of risk, and it is tempting to wonder what would have happened if he had lent his services to the English government. Instead, on April 9, 1694, a different fate was set in motion. He killed a man in a duel, or brawl—the distinction, as Buchan explains, was not all that clear. “Duels then were not the tournaments of the Middle Ages or the affairs of honour of later years, governed by written codes of conduct and discharged at dawn with pistols in some snowy forest clearing,” he writes. They might be conducted “with rapiers or short swords in hot or barely cooling blood, sometimes with seconds drawn and fighting, and shading away into assassination and armed robbery.” Law was sent to prison to await a murder trial. He used his connections to get out, as prisoners of means did, and fled abroad as an outlaw.

Law spent the next few years knocking around Europe, learning about gambling and finance, and writing a short book, “Money and Trade Considered,” which in many respects foreshadows modern theories about money. He became rich; like Littlefinger in “Game of Thrones,” Law seems to have been one of those men who had the knack of “rubbing two golden dragons together and breeding a third.” He bought a fancy house in The Hague and made a close study of the many Dutch innovations in finance, such as options trading and short selling. In 1713, he arrived in France, which was beset by a problem he was well suited to tackle.

The King of France, Louis XIV, was the preëminent monarch in Europe, but his government was crippled by debt. The usual costs of warfare were added to a huge bill for annuities—lifelong interest payments made in settlement of old loans. By 1715, the King had a hundred and sixty-five million livres in revenue from taxes and customs. Buchan does the math: “Spending on the army, the palaces and court and the public administration left just 48 million livres to meet interest payments on the debts accumulated by the illustrious kings who had gone before.” Unfortunately, the annual bill for annuities and wages of lifetime offices came to ninety million livres. There were also outstanding promissory notes, amounting to nine hundred million livres, left over from various wars; the King wouldn’t be able to borrow any more money unless he paid interest on those notes, and that would cost an additional fifty million livres a year. The government of France was broke.

In September of 1715, Louis XIV died, and his nephew the Duke of Orleans was left in charge of the country, as regent to the child king Louis XV. The Duke was quite something. “He was born bored,” the great diarist Saint-Simon, a friend of the Duke’s since childhood, observed. “He could not live except in a sort of torrent of business, at the head of an army, or in managing its supply, or in the blare and sparkle of a debauch.” Facing the financial crisis of the French state, the Duke started listening to the ideas of John Law. Those ideas—more or less orthodox policy today—were wildly original by the standards of the eighteenth century.

Law thought that the important thing about money wasn’t its inherent value; he didn’t believe it had any. “Money is not the value for which goods are exchanged, but the value by which they are exchanged,” he wrote. That is, money is the means by which you swap one set of stuff for another set of stuff. The crucial thing, Law thought, was to get money moving around the economy and to use it to stimulate trade and business. As Buchan writes, “Money must be turned to the service of trade, and lie at the discretion of the prince or parliament to vary according to the needs of trade. Such an idea, orthodox and even tedious for the past fifty years, was thought in the seventeenth century to be diabolical.”

This idea of Law’s led him to the idea of a new national French bank that took in gold and silver from the public and lent it back out in the form of paper money. The bank also took deposits in the form of government debt, cleverly allowing people to claim the full value of debts that were trading at heavy discounts: if you had a piece of paper saying the king owed you a thousand livres, you could get only, say, four hundred livres in the open market for it, but Law’s bank would credit you with the full thousand livres in paper money. This meant that the bank’s paper assets far outstripped the actual gold it had in store, making it a precursor of the “fractional-reserve banking” that’s normal today. Law’s bank had, by one estimate, about four times as much paper money in circulation as its gold and silver reserves. That is conservative by modern banking standards. A U.S. bank with assets under a hundred and twenty-four million dollars is obliged to keep a cash reserve of only three per cent.

Two dogs from different owners hug each other. “I guess you’re right—we have met before.” Cartoon by Lisa Rothstein The new paper money had an attractive feature: it was guaranteed to trade for a specific weight of silver, and, unlike coins, could not be melted down or devalued. Before long, the banknotes were trading at more than their value in silver, and Law was made Controller General of Finances, in charge of the entire French economy. He also persuaded the government to grant him a monopoly of trade with the French settlements in North America, in the form of the Mississippi Company. He funded the company the same way he had funded the bank, with deposits from the public swapped for shares. He then used the value of those shares, which rocketed from five hundred livres to ten thousand livres, to buy up the debts of the French King. The French economy, based on all those rents and annuities and wages, was swept away and replaced by what Law called his “new System of Finance.” The use of gold and silver was banned. Paper money was now “fiat” currency, underpinned by the authority of the bank and nothing else. At its peak, the company was priced at twice the entire productive capacity of France. As Buchan points out, that is the highest valuation any company has ever achieved anywhere in the world.

It ended in disaster. People started to wonder whether these suddenly lucrative investments were worth what they were supposed to be worth; then they started to worry, then to panic, then to demand their money back, then to riot when they couldn’t get it. Gold and silver were reinstated as money, the company was dissolved, and Law was fired, after a hundred and forty-five days in office. In 1720, he fled the country, ruined. He moved from Brussels to Copenhagen to Venice to London and back to Venice, where he died, broke, in 1729.

The great irony of Law’s life is that his ideas were, from the modern perspective, largely correct. The ships that went abroad on behalf of his great company began to turn a profit. The auditor who went through the company’s books concluded that it was entirely solvent—which isn’t surprising, when you consider that the lands it owned in America now produce trillions of dollars in economic value.

Today, we live in a version of John Law’s system. Every state in the developed world has a central bank that issues paper money, manipulates the supply of credit in the interest of commerce, uses fractional-reserve banking, and features joint-stock companies that pay dividends. All of these were brought to France, pretty much simultaneously, by John Law. His great and probably unavoidable mistake was to underestimate the volatility that his inventions introduced, especially the risks created by runaway credit. His period of brilliant success in France left only two monuments. One was created by the Duke of Bourbon, who cashed out his shares in the company and used the windfall to build the Great Stables at Chantilly. “John Law had dreamed of a well-nourished working population and magazines of home and foreign goods,” Buchan notes. “His monument is a cathedral to the horse.” His other legacy is the word “millionaire,” first coined in Paris to describe the early beneficiaries of Law’s dazzling scheme.

How did these once wild ideas become part of the very fabric of modern finance and government? Trial and error. It was not the case that smart people figured everything out at once and implemented it simultaneously, as Law tried to do. The modern economic system evolved, and evolution involves innovations, repetitions, failures, and dead ends. In finance, it involves busts and panics and crashes, because, as James Grant says in his lively new biography of the Victorian banker-journalist Walter Bagehot, “in finance and economics, we keep stepping on the same rakes.”

Bagehot (pronounced “badge-it”) knew all about those rakes. He grew up in the West of England in a family with strong links to a well-run local bank, Stuckey’s. After going to university and trying his hand at being a lawyer, he turned to journalism and to banking, the latter career paying for the former. He married the daughter of James Wilson, who had founded The Economist, in 1843—Bagehot became its third editor—and lived a life that was, from the outside, fairly uneventful. The interest in Bagehot comes from his dazzling, witty, paradox-loving writing, and in particular from his two key works, “The English Constitution” (1867), which sums up the unwritten order of Great Britain’s political institutions, and “Lombard Street” (1873), which explains how banking works. These books are still readable today, but they were of interest mainly to wonks until Ben Bernanke name-checked Bagehot as a crucial influence on the thinking behind the 2008 bank bailouts. That caused a revived interest, which led to the writing of Grant’s “Walter Bagehot: The Life and Times of the Greatest Victorian.”

“Greatest” is a loaded word, especially since Grant—who is, among other things, the founder of Grant’s Interest Rate Observer—makes it clear that Bagehot was an unashamed misogynist and racist (“There are breeds in the animal man just as in the animal dog”) and an accomplished hypocrite. The last quality was useful from the journalistic point of view; Bagehot was brilliant at swapping sides without ever admitting that he had changed his mind. A Confederate victory in the Civil War, for instance, was “a certain fact,” and President Lincoln was “dishonest and foolish,” a settled view that didn’t preclude Bagehot from declaring, once the Union had prevailed, that “panic did not for a moment unnerve the iron courage of the American democracy.” His subsequent elegy for Lincoln is a genuinely lovely piece of writing: “Difficulties, instead of irritating him as they do most men, only increased his reliance on patience; opposition, instead of ulcerating, only made him more tolerant and determined.”

In a sense, this highfalutin hypocrisy and lack of principle is the point of Bagehot. His work on the English constitution focussed on a paradox: the pomp and circumstance of monarchy had an important function, he argued, precisely because the monarch had no real power. Bagehot’s work on banking similarly focussed on the difference between appearances and realities, specifically the gap between the air of solidity and respectability cultivated by Victorian banks and the evident fact that they kept collapsing and going broke. There were huge bank crises in 1797, in 1825, in 1847, and in 1857, all of them caused by the oldest and simplest reason of bankruptcy in finance: lending money to people who can’t pay it back.

In theory, all the money in circulation during the era of Victorian banking was backed up by deposits in gold. One pound in paper money was backed by 123.25 grains of actual gold. In practice, that wasn’t true. There were multiple occasions—usually linked to the cost of that old classic, war with France—when the government suspended the convertibility of paper money to gold. In addition, banks could print their own money. They often didn’t have enough gold to sustain the value of their notes, in the event of customers coming to the bank and demanding conversion. That phenomenon, the dreaded “bank run,” was a direct outcome of the fractional-reserve banking prefigured by John Law. A system in which banks don’t hold cash reserves equivalent to their outstanding loans works fine, unless enough people turn up at the bank and simultaneously want their paper money turned into its metal equivalent. Unfortunately, that kept happening, and banks kept going broke. The issues at stake were the same as those that had shaped the career of John Law, and which are on people’s minds again today: What is money? Where does it derive its value? Who finally guarantees the value of debts and credits?

Bagehot had answers to all those questions. He thought that money, real money, was gold, and gold alone. All the other forms of currency in the system were merely different kinds of credit. Credit was indispensable to a functioning economy, and helped make everybody rich, but in the final analysis only gold was legal tender, according to the strict definition of the term—money that cannot be refused in settlement of a debt. (U.S. currency makes sure you know it is legal tender: it says so right there on the front.) Bagehot loved a paradox, and this was one: all the credit in the system was essential to the economy, but it wasn’t really money, because it wasn’t gold, which underpinned the value of everything else.

So where was all the gold? In the Bank of England. The role of that once private company had evolved. Bagehot thought it was the Bank of England’s job to hold the gold, so that all the smaller banks didn’t have to. Instead, the smaller banks took deposits, made loans, and issued paper money. If they got into trouble—which they tended to do—the big bank would bail them out. Why shouldn’t all the other banks hold their own gold, and take care of their own solvency? Bagehot the banker-writer was completely frank about the reason. “The main source of the profitableness of established banking is the smallness of the requisite capital,” he wrote. The modern way of putting this would be to talk about the bank’s return on equity. The less equity the bank needed to keep as a margin of safety, the more money it could lend, and, therefore, the more profit it could make. Gold was essential in order to guarantee the currency, but the bankers didn’t want it taking up valuable space on their balance sheets. Better to let the government do that, in the form of the Bank of England.

We still have a version of this system, in which government guarantees underpin the profitability of banks. The central bank’s crucial role is to lend money freely at a time of crisis—to be what is called “the lender of last resort.” Grant, who admits to “a libertarian’s biases,” sees this doctrine as the seed of “deposit insurance, the too-big-to-fail doctrine, and the rest of the modern machinery of socialized financial risk.”

Like John Law and Walter Bagehot, I’m the child of a man who worked in a bank, and, as such, I had a banker’s-son question running through my mind as I read Grant’s entertaining book: what happened to Bagehot’s bank? The answer is that Stuckey’s was taken over by another bank, Parr’s, in 1909. Parr’s was part of the larger National Westminster Bank, which was taken over by the Royal Bank of Scotland, in 2000. R.B.S., as it is unaffectionately known in the U.K., grew through takeovers to become, in the early years of this century, the biggest company in the world, as measured by the size of its balance sheet. Then came the credit crunch, and the moment—the latest version of the old familiar one—when things turned out not to be worth what they were supposed to be worth. The biggest bank in the world came, according to its chairman, to within “a couple of hours” of complete collapse. The outcome was a huge bailout, and the nationalization of R.B.S., with costs to the British taxpayer of forty-five billion pounds. Not much about that story would have surprised John Law or Walter Bagehot. Maybe, though, both men—the man who almost bankrupted a country and the supreme advocate of bankers’ bailouts—would be amused to see just how little we have learned. As for the question of what to do about the bankers responsible for the crash, Kublai Khan would probably have had some ideas.